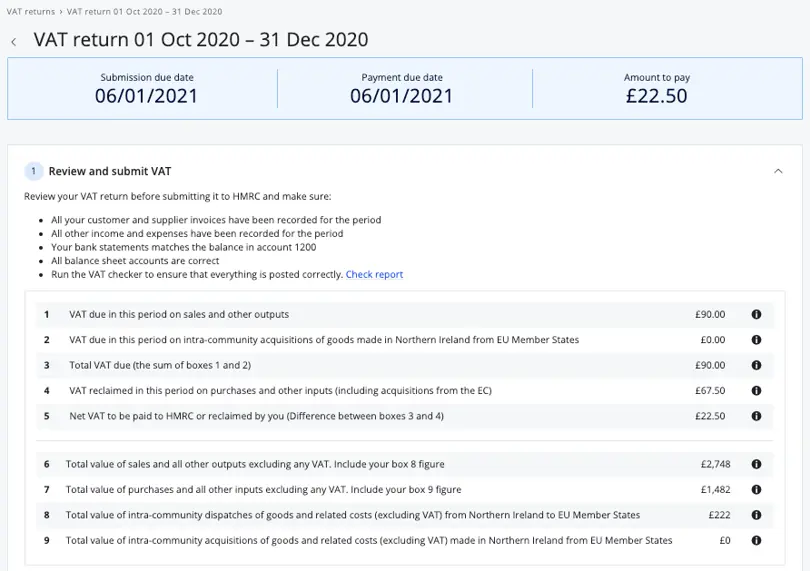

How to understand and review your VAT return

When you submit your VAT return, you can find your automated return in Reports → VAT Returns. The VAT return is automatically generated from the bookkeeping you have done in Bokio.

You should review your VAT return before submitting it to HMRC to make sure that all your invoices, income and expenses have been recorded for the period.

The best way to do this is to click on the information buttons next to each box on the VAT Returns.

You will then see a breakdown of all the journal entries that make up the total on the particular VAT box that you have clicked on. This allows you to ensure that no transactions have been omitted or duplicated.

This can also be exported to Excel for further investigations or to be sent to HMRC for VAT investigations.

You should also check your bank statements match the balance in account 1200 and that your balance sheet accounts are correct.

What does your VAT return mean?

Here is a run through of what your VAT return means:

1 VAT due in this period on sales and other outputs

The VAT added to your sales and other sources of income that you are required to pay to HMRC.

2 VAT due in this period on acquisitions from other EC Member States

Goods purchased from a supplier who are registered for VAT in another EU member state, and has therefore removed the VAT from their invoice. You include VAT at the rate that would have been charged in the UK and it is then reversed out in Box 4.

3 Total VAT due

The total of amounts ‘1’ and ‘2’.

4 VAT reclaimed in this period on purchases and other inputs (including acquisitions from the EC)

The VAT you can claim back on goods and services that you have purchased from suppliers for your business, including VAT on purchases from EU member states. This is included in Box 2 and removed by the supplier from the invoice because they are registered for VAT in their country.

5 Net VAT to be paid to HMRC or reclaimed by you

The difference between amounts ‘3’ and ‘4’. This will show if you need to pay HMRC VAT after filing your return, or if you can reclaim money from HMRC.

6 Total value of sales and all other outputs excluding any VAT

The whole value of all your sales (goods and services) excluding VAT, both inside and outside the UK. This includes the total from amount ‘8’.

7 Total value of purchases and all other inputs excluding any VAT

The total value of all goods and services you have purchased from suppliers, excluding VAT, from both inside and outside the UK. This will include the total from amount ‘9’.

8 Total value of all supplies of goods and related costs, excluding any VAT, to other EC Member States

The total value of all goods you sell (excluding VAT) to another EU member state.

9 Total value of all acquisitions of goods and related costs, excluding any VAT, from other EC Member States

The total value of all goods you buy (excluding VAT) from another EU member state, which then enter the UK.